When Is Medicare Primary Insurance?

After becoming eligible for Medicare, some people may find themselves enrolled in multiple insurance plans. Employer-sponsored healthcare, Medicaid and retiree health plans are common forms of coverage for seniors who are also enrolled in Medicare Part A and Part B.

Medicare works with other forms of insurance in different ways. It's important to understand when Medicare is your primary insurance and when it is not. This helps ensure that your covered healthcare bills are paid properly and reduces confusion when it's time to pay your out-of-pocket costs.

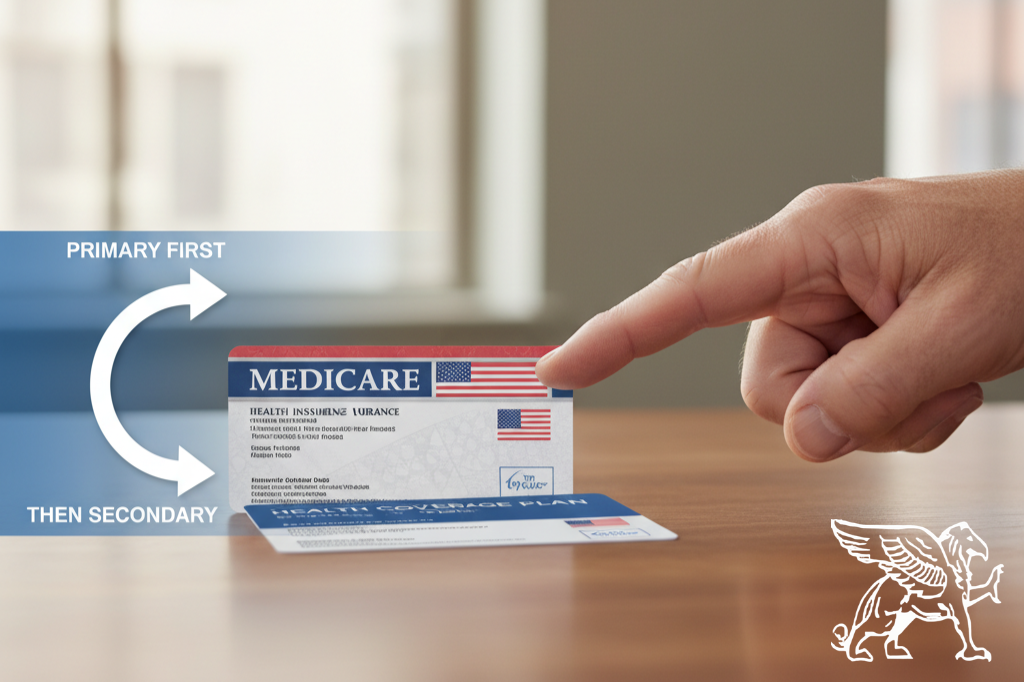

Primary vs. secondary insurance

If you have multiple insurance plans, one of those will be the primary payer. This means that the plan will pay its benefits first. Then, the secondary form of insurance will pay next. Typically, secondary insurance pays some or all of the remaining costs. After the primary and secondary insurance plans pay, the remaining costs are passed to you, the policy holder.

The Center for Medicare Services (CMS) has a predetermined set of rules that coordinates when Medicare serves as the primary insurance. It's important to learn which forms of insurance are primary or secondary with Medicare — especially if you're enrolling in Medicare for the first time. Some insurance plans won't pay if you are eligible for Medicare. If you haven't enrolled, you may not get the coverage you're expecting!

When Medicare acts as the primary insurance

In most cases, Medicare becomes your primary form of insurance as soon as you're eligible to enroll in Medicare Parts A and B. Medicare is primary when:

- Medicare is your only form of insurance: If you're only enrolled in Medicare, Part A and Part B (or Medicare Advantage if you're enrolled in a plan) is your primary insurance by default.

- You have Medicare and a Medigap policy: If you've enrolled in Original Medicare and have purchased a Medigap plan, Medicare is your primary insurance. The Medigap plan is secondary and pays for some or all of the costs remaining after Part A and Part B pay their share.

- You have a group plan from an employer with fewer than 20 employees: If you have a group health insurance plan from your current employer, pay close attention to the size of the company. Medicare is primary to group plans from small businesses with fewer than 20 employees. You'll want to enroll in Medicare as soon as you're eligible to ensure the Medicare plan pays first.

- You have Medicaid: If you are eligible for Medicare and are also covered by Medicaid, Medicare pays first.

- You have retiree coverage: Retiree insurance becomes secondary to Medicare as soon as you turn 65 and become eligible for Medicare.

- You have COBRA: If you enroll in COBRA after you've become eligible for Medicare, Medicare is primary.

When Medicare is secondary insurance

Medicare is secondary in only a few situations:

- You have a group plan from an employer with 20 employees or more: Medium to large businesses that offer group health insurance plans work differently. If you have a group plan from an employer with more than 20 employees, Medicare is secondary to your group plan. This is why some seniors are able to delay enrollment in Medicare Part B while they have employer-sponsored coverage.

- You have workers' compensation: Workers' compensation insurance is primary to Medicare for any services related to the workers' compensation claim. However, Medicare is still primary for general healthcare services unrelated to the claim.

Determining your primary insurance status

If you aren't sure whether Medicare or your other insurance plans are primary, you'll want to refer to your policies' benefit materials and/or contact the CMS Benefits Coordination & Recovery Center. Informing Medicare about other forms of insurance you have is critical in determining the order your plans will pay.

Ready to learn more about how Medicare works? PlanEnroll can help. Contact us today to speak with a licensed insurance agent.

Griffin Consulting

Griffin Consulting